Social Market Analytics, Inc. (SMA) aggregates the intentions of professional investors as expressed on Twitter & StockTwits and publishes a series of metrics that describes the current conversation relative to historical benchmarks. Our data is a leading indicator of price movement both positive and negative.

There is unique predictive information in unstructured content. Social Market Analytics use AI and Machine Learning techniques developed over the last eight years to convert this unstructured content into data suitable for quantitative analysis. This opens a whole new area of big data analysis.

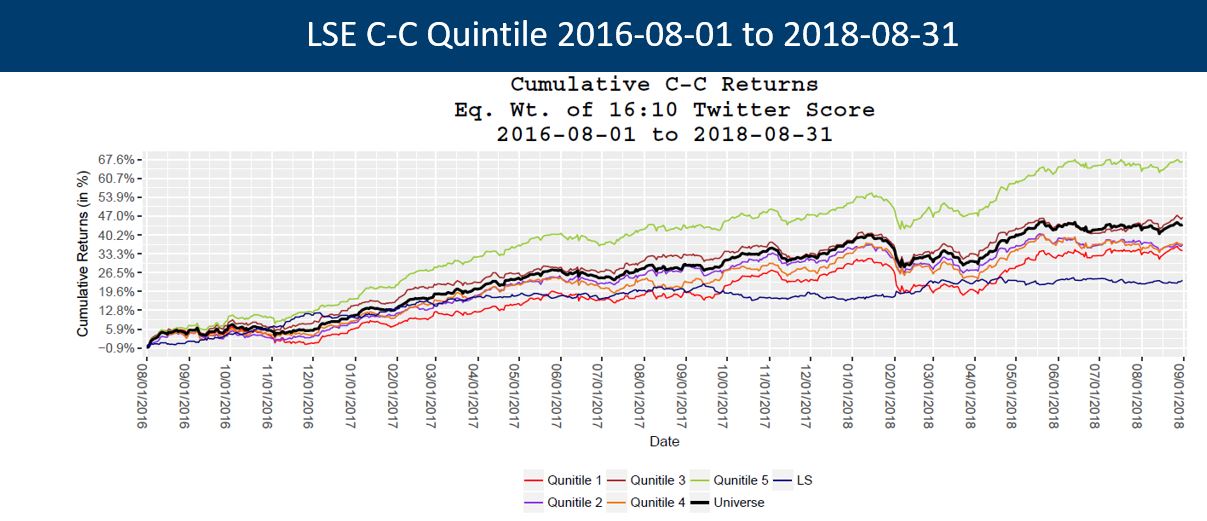

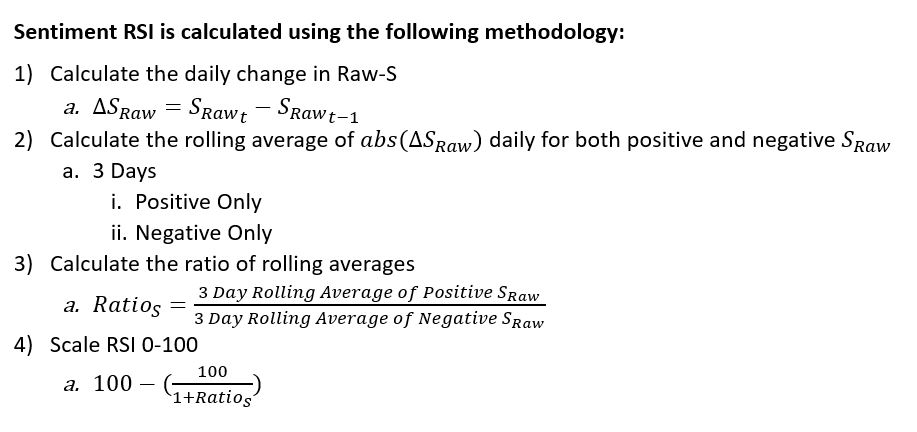

Social Market Analytics (SMA) calculates predictive sentiment on the entire US equity universe, Currencies, Commodities, Crypto currencies, ETF’s and custom sources. This blog is about the predictive nature of our LSE security universe. We calculate our custom metrics on the top 1000 market cap securities listed on the LSE. Our LSE data starts on 1/1/2016. Below is a cumulative quintile distribution of returns based on our S-Score metrics. Our S-Score is effectively a Z-Score comparing 24-hour sentiment based on the Tweets of professional investors compared to a 20-day baseline. Prediction periods vary per asset class and baseline. Longer baseline comparisons lead to longer prediction periods.

Stocks with abnormally positive conversations typically outperform their peers and stocks with abnormally negative conversations typically underperform their peers. As expected conversations with normal positive or negative tones perform like the overall market.

Below is a typical quintile chart for the LSE 1000 universe tracked from post Brexit to 8/31/2018. The spread between the top and bottom quintiles is 10% annualized. Sharpe and Sortino ratios are in the table below that. To learn more or request a historical data set contact SMA with any questions ContactUS@SocialMarketAnalytics.com