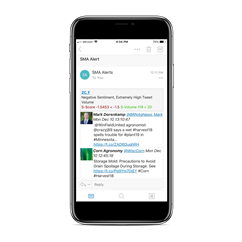

Social Market Analytics (SMA) tracks real-time sentiment on equities, commodities, currencies, ETF’s and crypto currencies. SMA has the most powerful and customizable Alerting API combining Twitter sentiment and pricing metrics. Users receive custom real-time sentiment alerts on instruments in their watch list. For example, on December 11, 2018, SMA’s alerting system sent an alert on Corn at 12:12 pm CT when corn was @ $385.25. Below is the email and mobile alert.

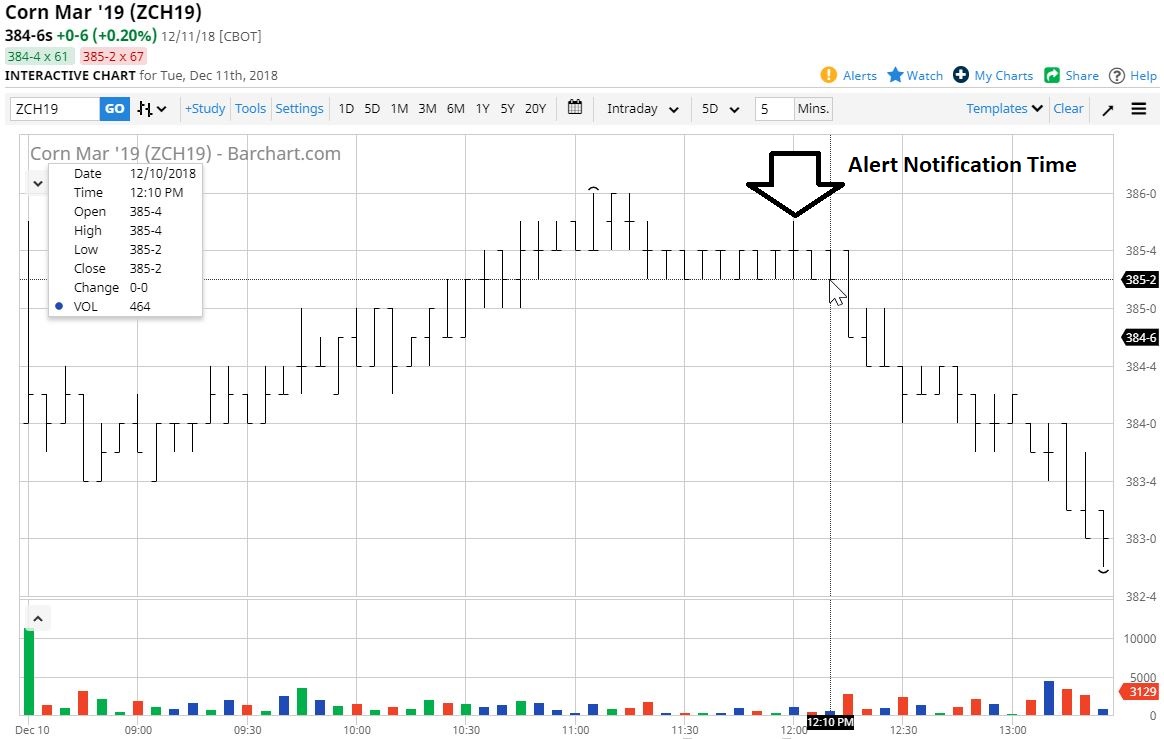

Subsequent to the alert, corn moved lower starting at 12:17pm CT. The price continued to move lower the remainder of the day and closed at $383.25. (See chart below)

The above alert was based on SMA’s rolling 24-hour sentiment. SMA also calculates a Long-term sentiment with longer price projection periods. Corn’s long-term S-Factor flipped from positive to negative on November 14th. 12/10 was the first day the long-term S-Factor for corn reached a significantly negative level of -1.5 standard deviations more negative than the longer-term baseline conversation. For more information please contactUs@SocialMarketAnalytics.com