Social Market Analytics aggregates the intentions of professional investors as expressed on Twitter. SMA factors are highly predictive over various time frames. In June of 2017 Social Market Analytics launched a weekly re-balanced large cap sentiment based index. This index is comprised of twenty-five stocks with the highest average Twitter sentiment over the prior week selected and re-balanced Friday afternoons from the CBOE Large Cap 450 Index. This index has been published daily since that date and is available on all major feeds.

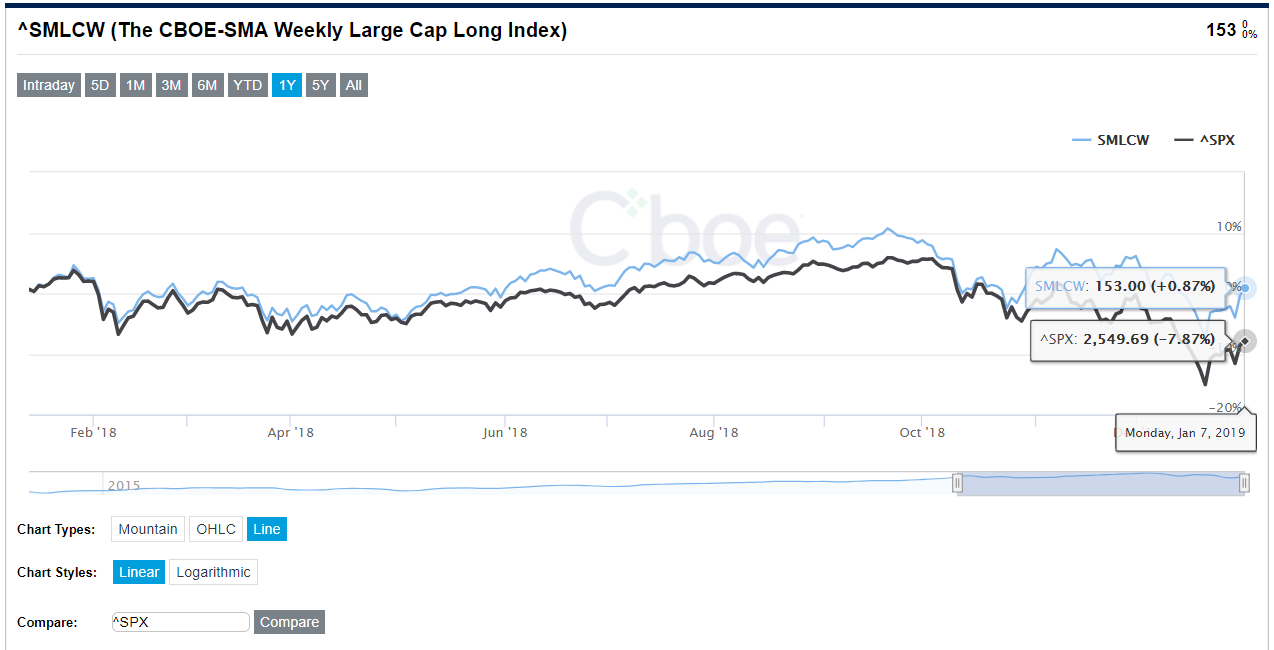

Last year the SP500 Index had a return of -8.4%. The CBOE SMLC Index had a return of +.87%. Below is a comparative return chart over the last year compared to the SP500.

For more information or to license this index please contact us at ContactUs@SocialMarketAnalytics.com