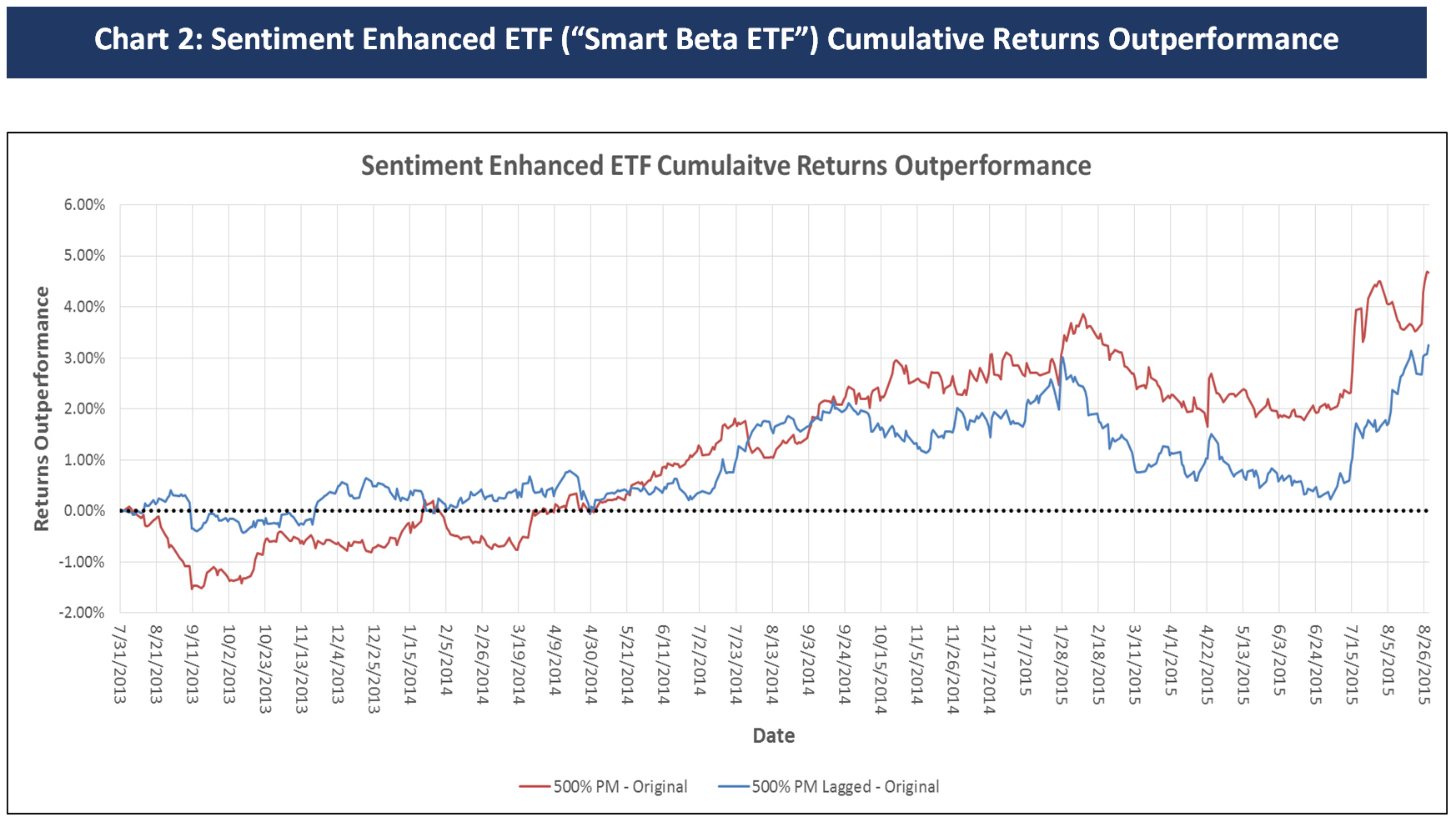

General Market Indicator: Volatility of Sentiment Helpful in Predicting Overall Market Performance

/The target of this research was to find an indicator that helps predict the direction of the overall US Equity market for the next week using sentiment data from the previous week. The hypothesis is when there is high volatility in sentiment over the previous week, which means investors have differing opinions, the subsequent week overall market performance will underperform. When volatility on sentiment is low or neutral, the crowd has reached a consensus and the general market will outperform over the next week. The sentiment metric used to represent volatility is Raw-Volatility in SMA’s S-Factor data feed, which captures the volatility of the sentiment from Twitter conversations. All Raw-Volatility data points were taken from the 3:40 pm ET timestamp (20 minutes before the market close). We calculated the summation of Raw-Volatility for each date as a proxy to represent the volatility of Twitter social sentiment on the entire market. The exact calculation is as follows, where “N” is the number of companies with sentiment on that date and “D” is the date:

![]()

We then created a 7-day standardized volatility using a 91-day benchmark:

![]()

This Z_Volatility score follows a roughly normal distribution.

Using the S&P 500 ETF Trust (SPY) as a proxy of general market performance, we then look at the relationship between Z_Volatility and SPY’s return series. The daily close-to-close return is calculated as:

![]()

Hypothesis: When Z_Volatility for the previous closing Date is high, the subsequent market performance will be lower. When Z_Volatility is low or neutral, the next day’s market performance will be higher.

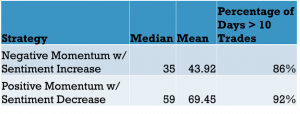

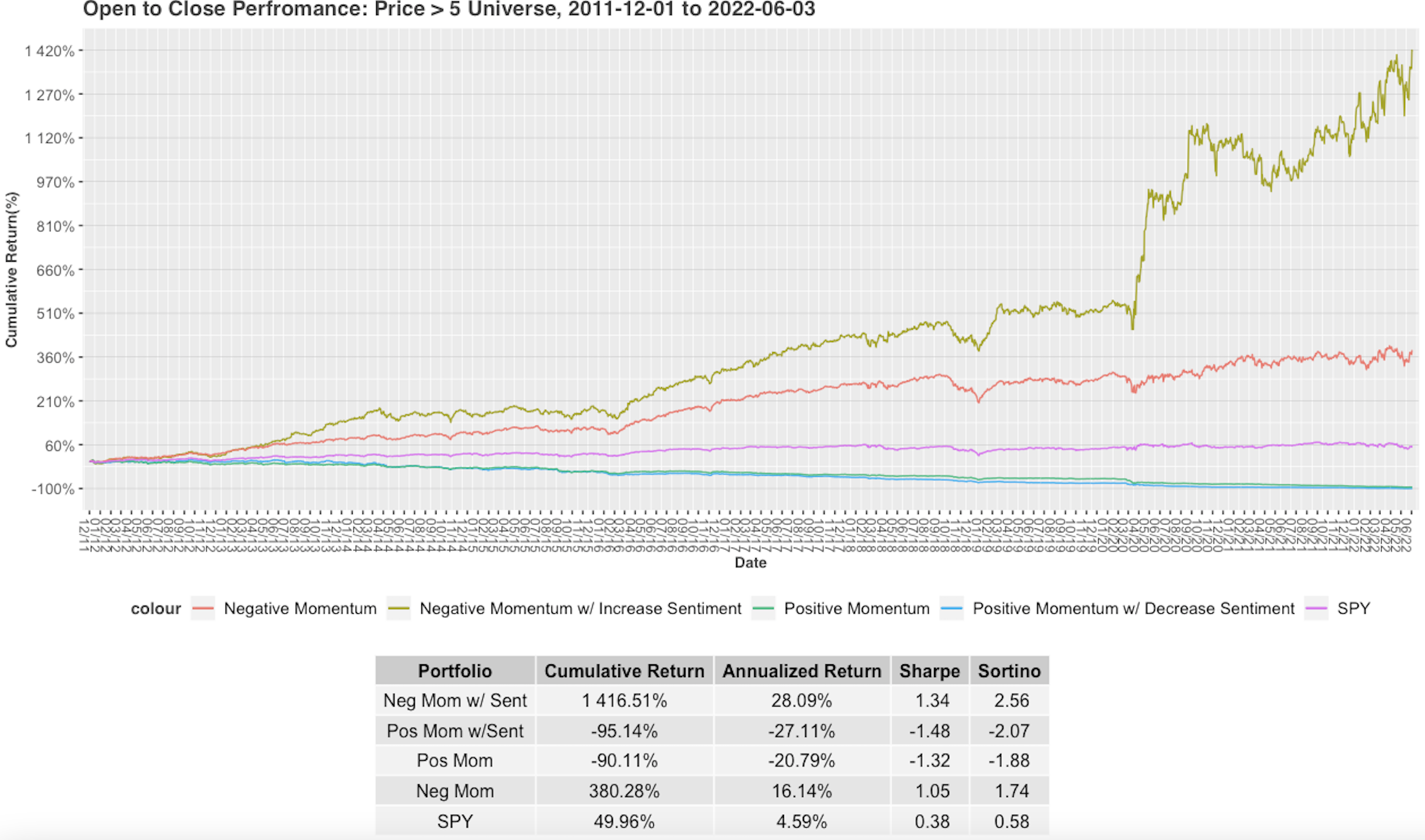

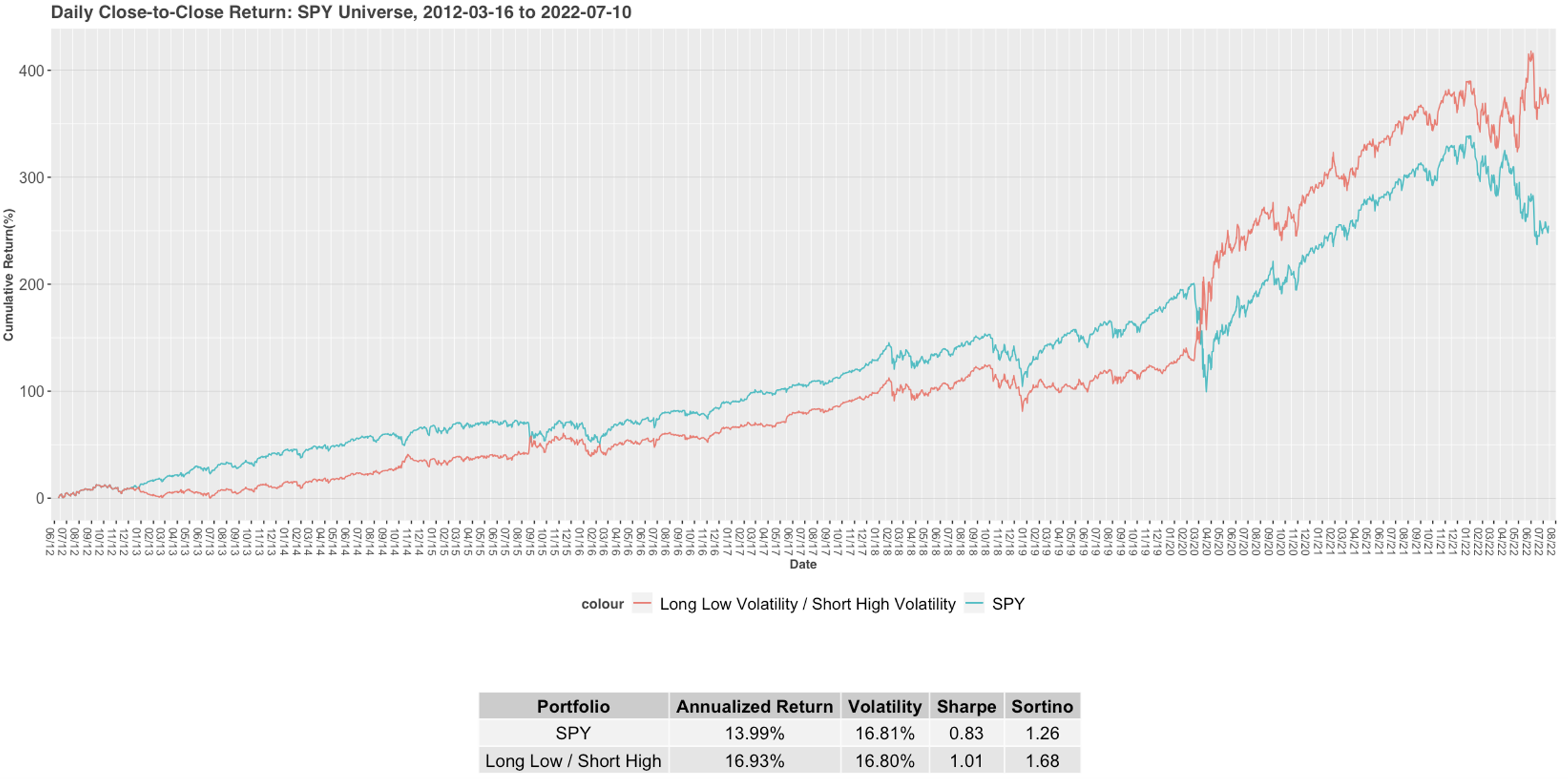

To test this, our strategy is to open short position of SPY when Z_Volatility > 1. When Z_Volatiltiy is =< 1, the portfolio treats SPY as a long position. This hypothetical portfolio is then compared to SPY over the past 10 years:

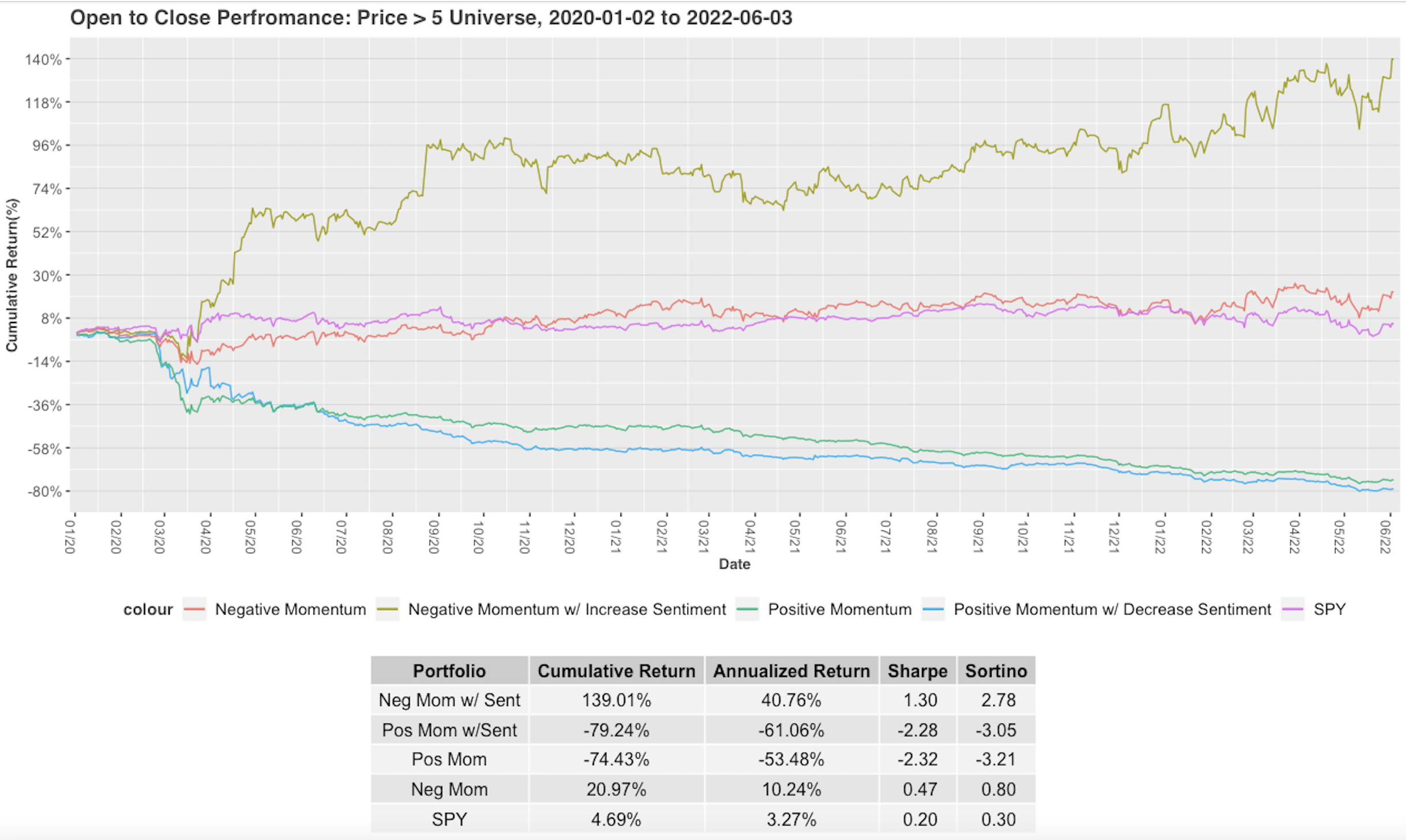

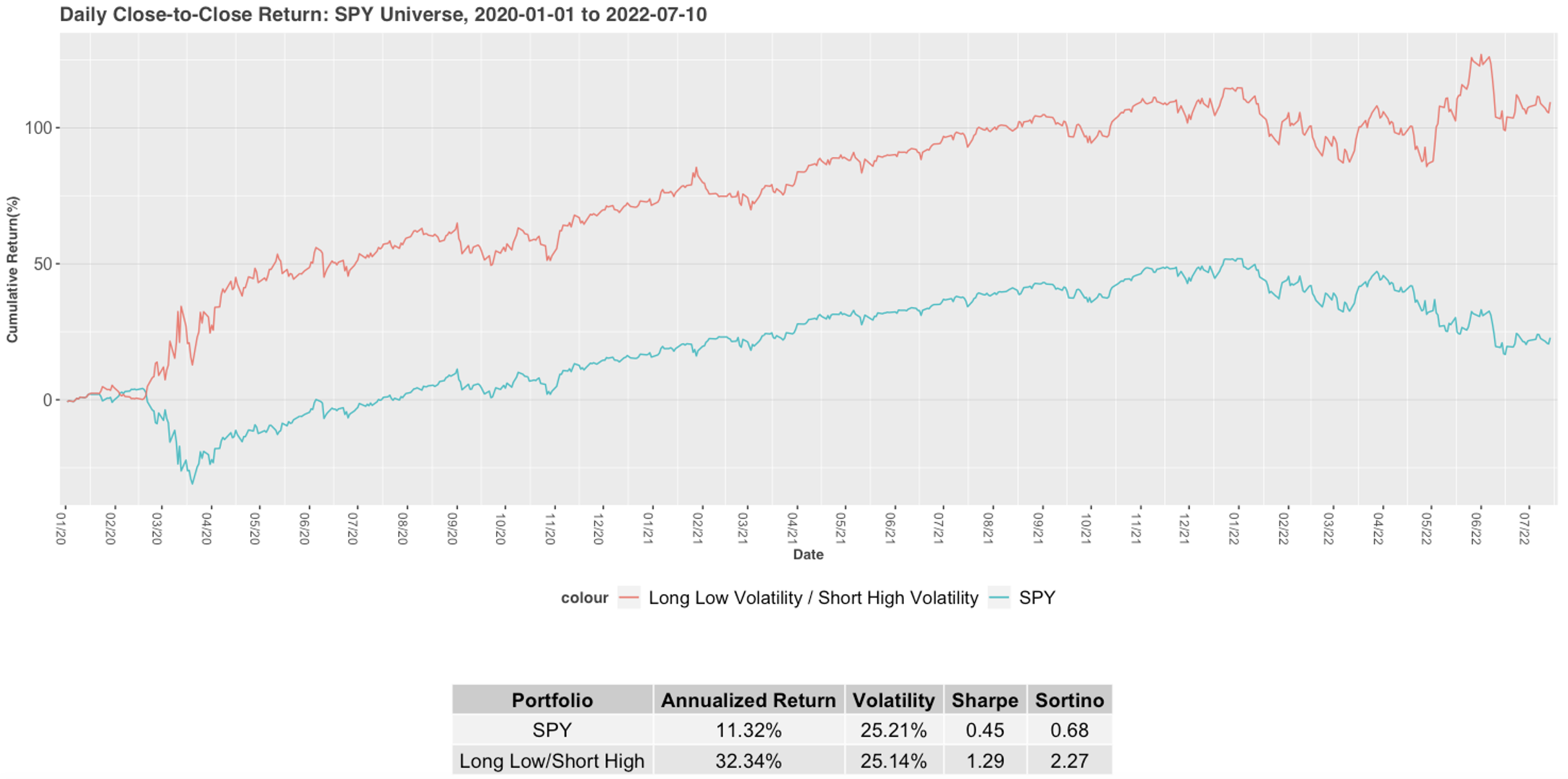

Prior to the COVID-19 pandemic, which began in early 2020, SPY outperformed the modified portfolio. However, since then the behavior of this factor changed drastically. Here is the same graph as above starting in 2020:

Taking a closer look, the separation since the beginning of 2020 is quite significant. Adding a short position to SPY when volatility on sentiment is high, has enhanced the portfolio’s return. Even though many of the days will maintain a long position, the Z-Volatility is predictive of downturns in the market since 2020. Traders could use this metric as an indicator to stay out of the market, or at the very least trade with more caution. The COVID-19 Pandemic led to a large amount of uncertainty surrounding the stock market and the direction its heading. A high Z_Volatility score indicates the public’s opinion is more uncertain about the direction of various stocks. This research shows the value of sentiment from Social Market Analytics in predicting macro-level events and price movements.

If you are interested in learning more about how SMA’s S-Factor data can help your trading strategies, please email us at contactus@socialmarketanalytics.com or schedule a demo using this link.