Social media is a new and rich source of trading ideas. To illustrate this point, below are some recent trading opportunities social media data presented. In each case activity and sentiment increase prior to the actual event. Social media is a leading indicator of stock performance and SMA is the leader in providing metrics based on social media.

Teva acquires Allergen

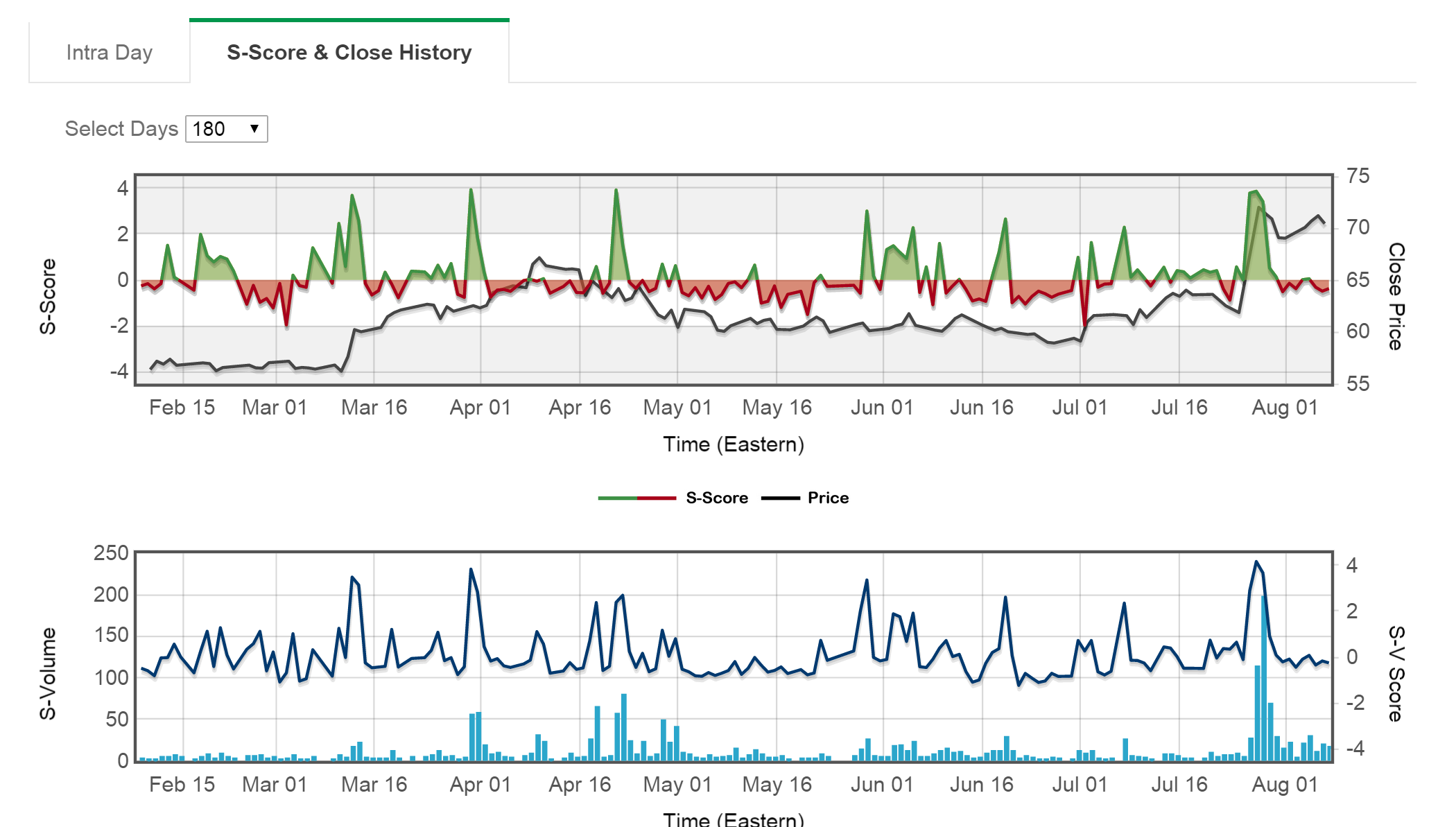

Teva Pharmaceutical Industries surged in pre-market trading on July 27, 2015 on news that the company will be acquiring Allergan’s (AGN) generic drug business. Before this happened, sentiment on Twitter had already become strongly positive. At 4:00 AM EDT, when the stock price was $66.00 there was significant positive sentiment on Twitter. The sentiment rapidly shifted positive. By 7:24 a.m., the stock was trading at $72.30. The stock opened at $67.80 when the sentiment was 3.92 and closed at $72.

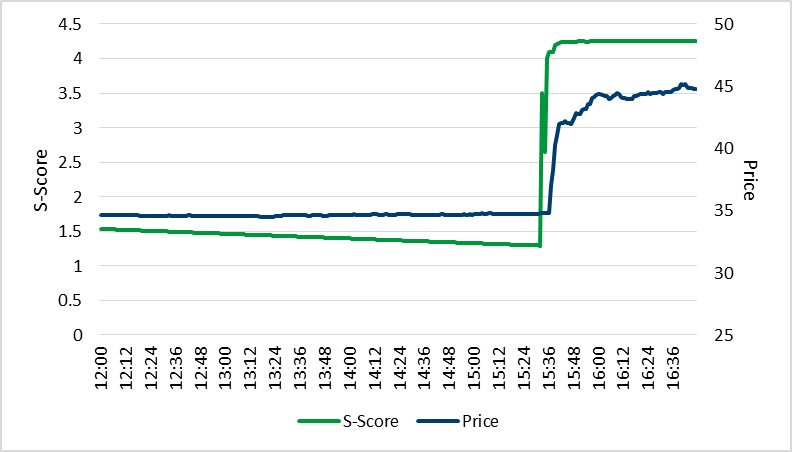

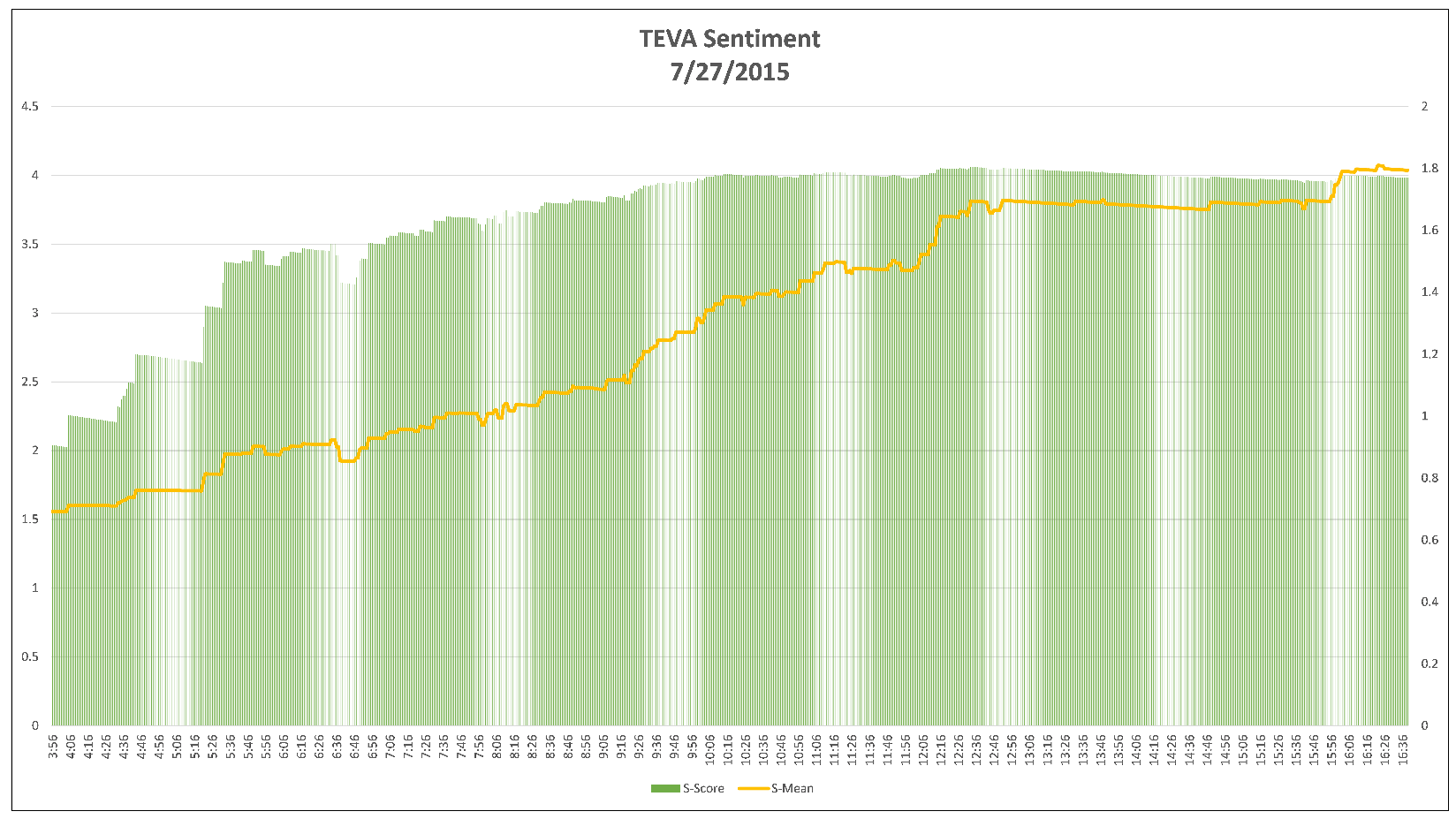

Figure 1: S-Score™ For TEVA Pre- and Post-Announcement.

Historically, daily sentiment scores for TEVA fluctuated near 0 (Neutral), with low social media activity as indicated by the time series of the S-Volume™ metric. This behavior started to change on July 26 with significant upticks in indicative Tweet volumes and sentiment levels. On the morning of July 27th,TEVA’s S-Score™ increased sharply to a high positve level, coincident with a spike in S-Volume™ consistent with high social media activity, indicating that SMA’s processing technology had sucessfully detected the signature of positve sentiment for TEVA embedded in the Twitter data stream. This high positive sentiment level persisted through the open on July 28th and then started to return to typical historical levels as the markets and social media fully integrated the effect of the announcement.

Rumored Announcement of Acquisition: Twitter (TWTR)

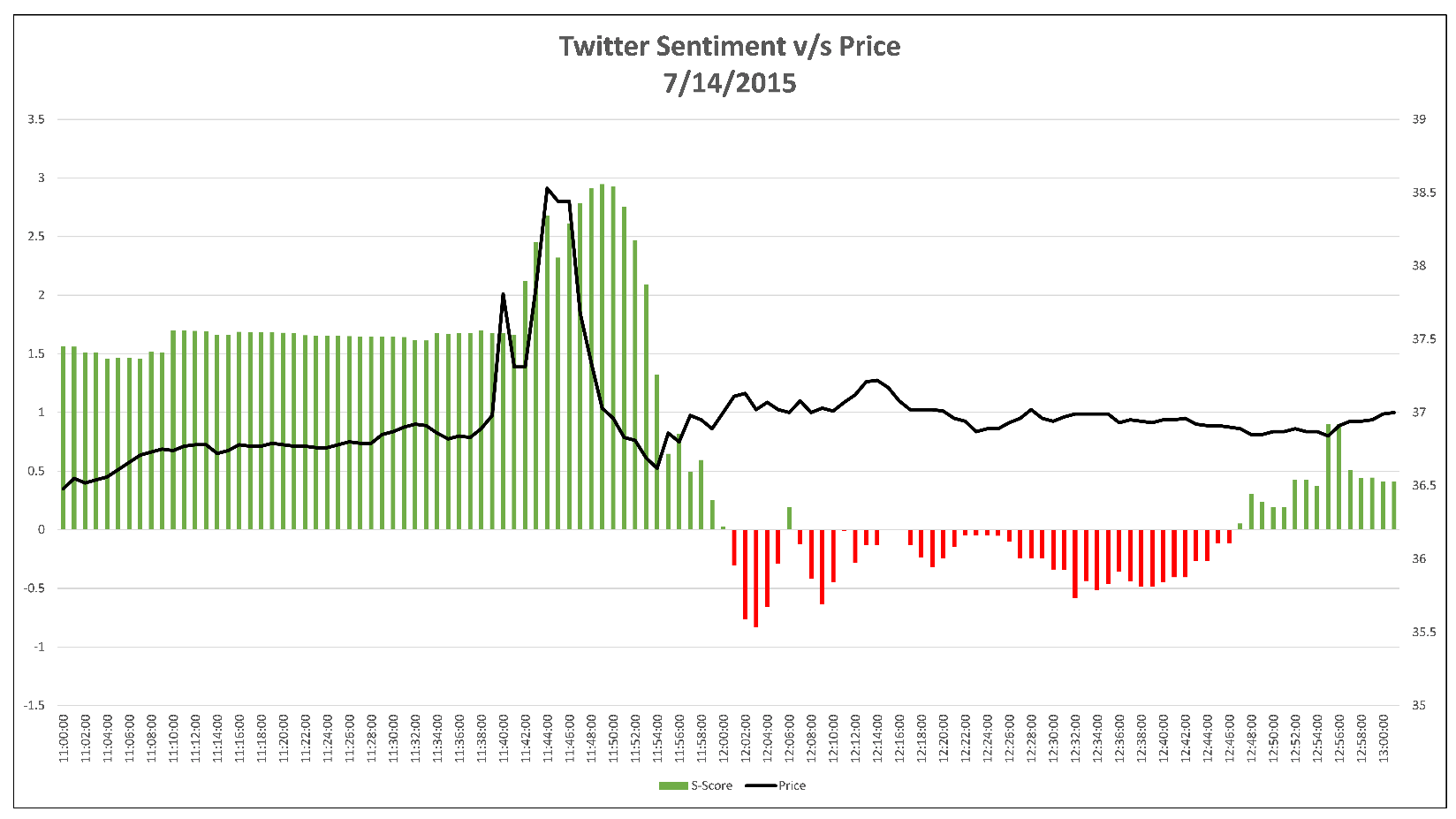

On July 14, 2015 at 11:39 AM EDT, a rumor started spreading on Twitter about Twitter being acquired by Bloomberg. At 11:40 AM, there was a Tweet from user ‘beckyhiu’ indicating that Bloomberg had offered $31 Billion to buy Twitter and that Twitter was considering the offer. This rumor caused the stock price to rise rapidly. A Tweet, about 30 seconds later, at 11.41 AM, by ‘zerosum24’ confirmed that the rumor had reached Twitter and people had started talking about it. The sentiment had started rising rapidly by this time. The changes in S-ScoreTM and S-DeltaTM were significantly positive. At 11:42 AM, the sentiment was over 2, and was statistically significant.

It was soon realized this might be a hoax and that no offer was made. At 11:42 AM, ‘TurboResearch’ questioned the credibility of the buyout offer.

There had been no official statement from Bloomberg, and hence, both the sentiment and the stock price kept rising. At around 11:50 AM, a journalist from Bloomberg Tweeted that the news was a hoax and that it was not to be believed. At this point sentiment started declining as people starting tweeting negatively. The stock price dropped rapidly. After that, there were mostly negative comments driven by the refuted rumor. The figures below show SMA sentiment factors leading the stock price quite accurately.

Figure 2: TWTR S-ScoreTM vs. Price

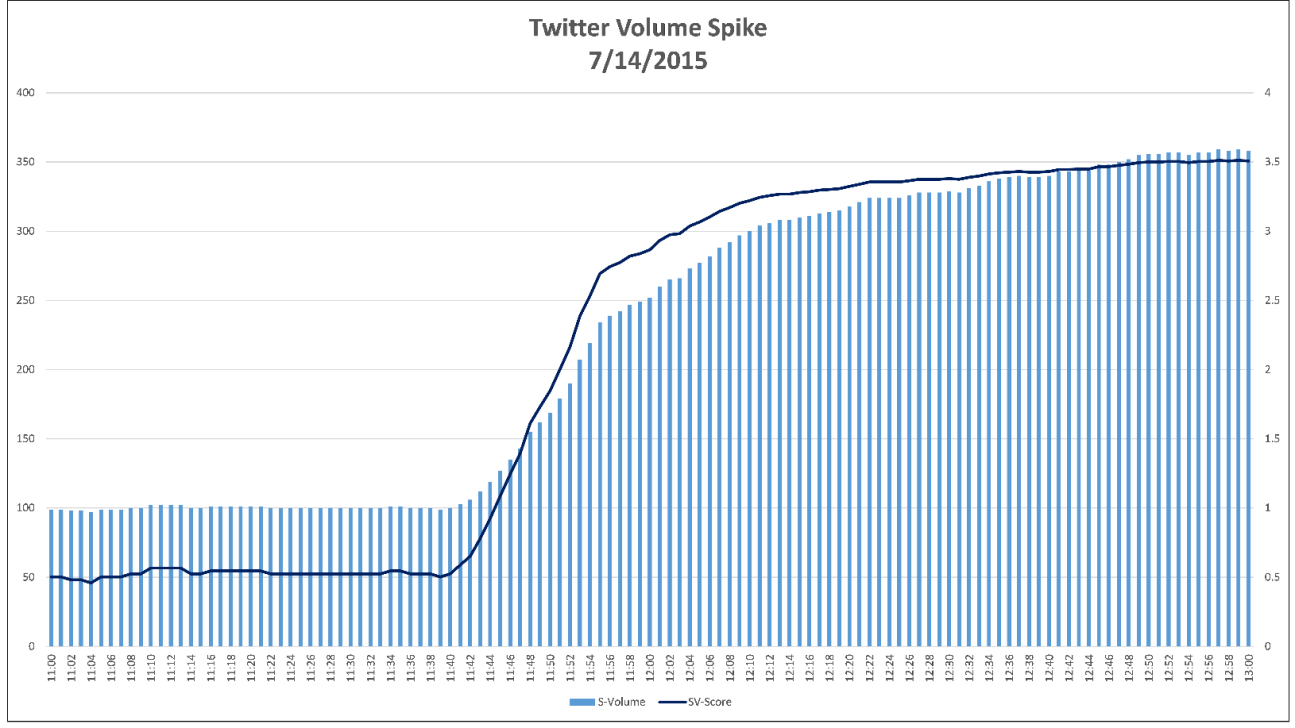

Figure 3: Intraday S-Volume™ Chart for TWTR

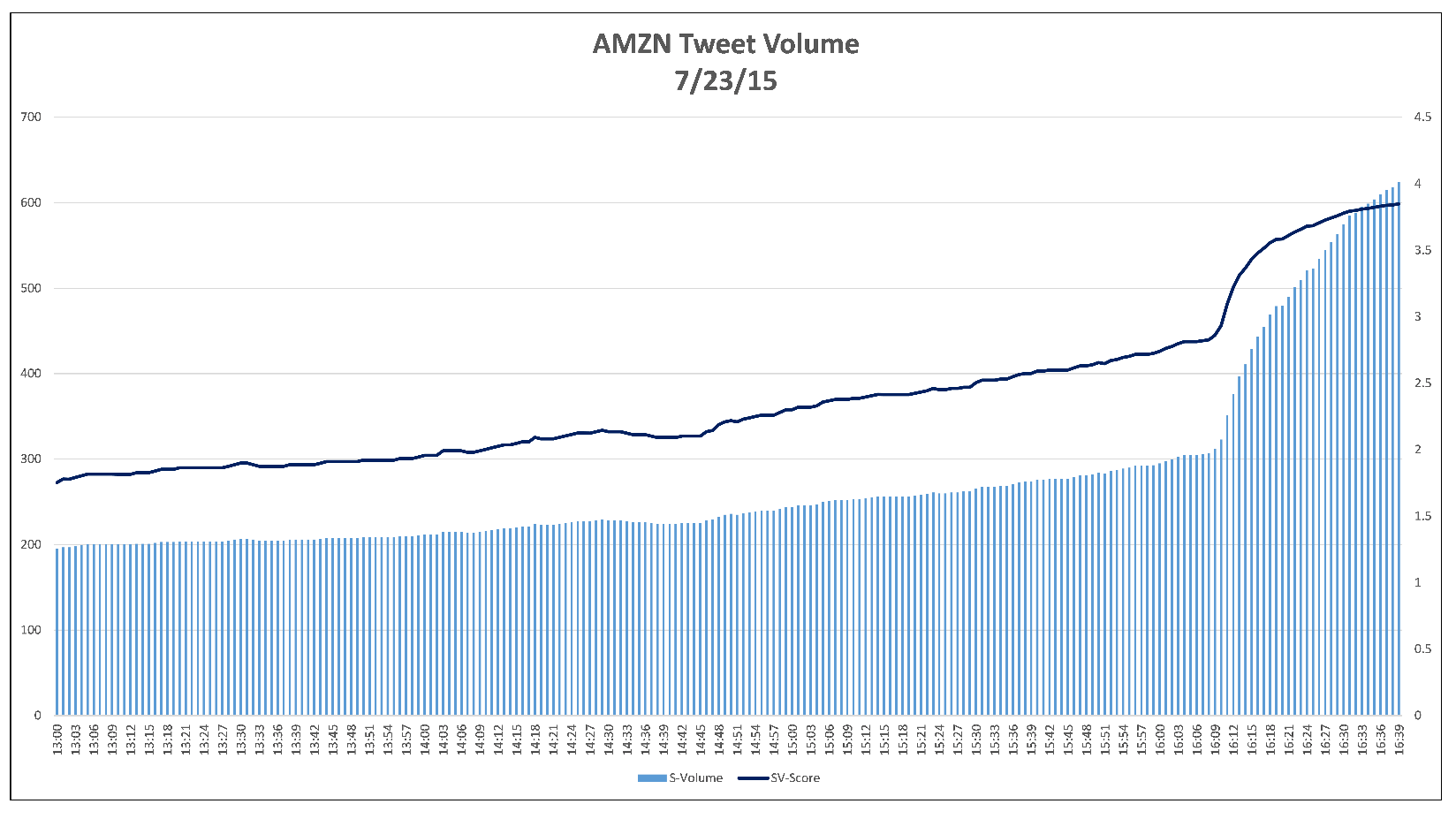

Amazon (AMZN) Earnings Announcement

Twitter sentiment can predict stock changes even after market close, as in the case of Amazon. Amazon reported earnings on July 23, 2015. While the market consensus was that the company would not beat expectations, the conversation on social media was different.

SMA data showed a sharp increase in sentiment metrics around 2:49 PM EDT. By 2:51 PM, the sentiment on Amazon was two standard deviations higher than its typical level. The stock was trading at $480.45 at this point. At market close, it traded at $482.18, higher than the price at the time when sentiment on Amazon became positive.

It was interesting to see how the stock traded after-hours once the company reported earnings. Amazon’s stock shot up more than 17% — to $568 — from its price at 3:51 PM EDT after the company reported a surprise quarterly profit. The hidden sentiment value in Twitter data predicted what “conventional” market speculators failed to predict.

Figure 4: Intraday S-Score™ And S-Volume™ Behavior across Amazon’s Earnings Event.

The progression of intraday S-Score™ and S-Volume™ metrics for Amazon is shown above from 1:00 PM EDT to 4:25 PM EDT. Amazon’s sentiment remained positive throughout the day and became significant around 2:50 PM. The sentiment saw a sharp rise post the earnings announcement after market close.

We publish our own research and analysis. We invite you to check our Research site for new updates and publications.

Thanks,

Joe