In this video we explain how our S-Factor feed uses the Twitter firehose to build trading signals, dashboards and widgets to help investors increase alpha. To find out how SMA can help your firm, email us at ContactUs@SocialMarketAnalytics.com or schedule a meeting using our 1 on 1 Meeting Signup.

Posts

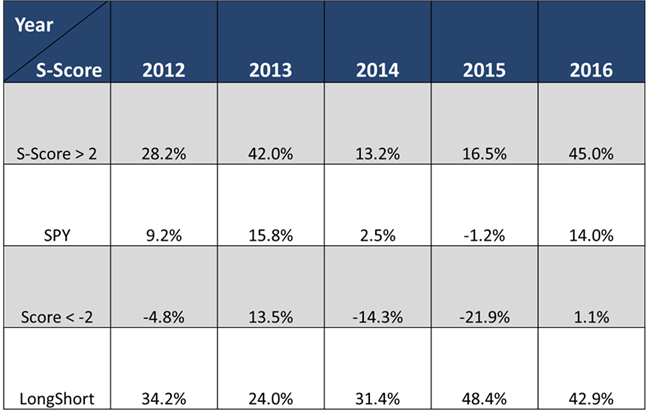

Last year was a good year for SMA data. High sentiment securities outperformed and low sentiment securities underperformed with good Sharpe’s and Sortino’s. The below tables contain returns and Sharpe/Sortino ratios for the full history of Social Market Analytics S-Factor data. Correlations to standard factors continue to be near zero. I’m sure our data can help in your investment process, contact us to learn more.

Five-year return summary:

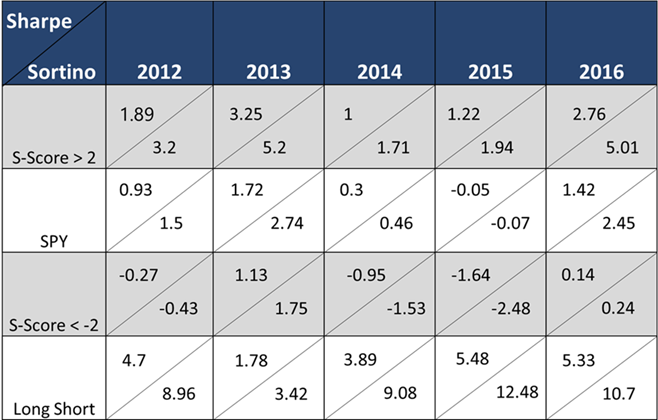

Sharpe / Sortino

Social media beats the mainstream media on a regular basis. Last week social media beat the news wire in reporting the MSFT acquisition of LNKD (blog post below) and Tuesday Twitter broke SCTY being acquired by TSLA. This information is not theoretical – it is actionable data in our feed!

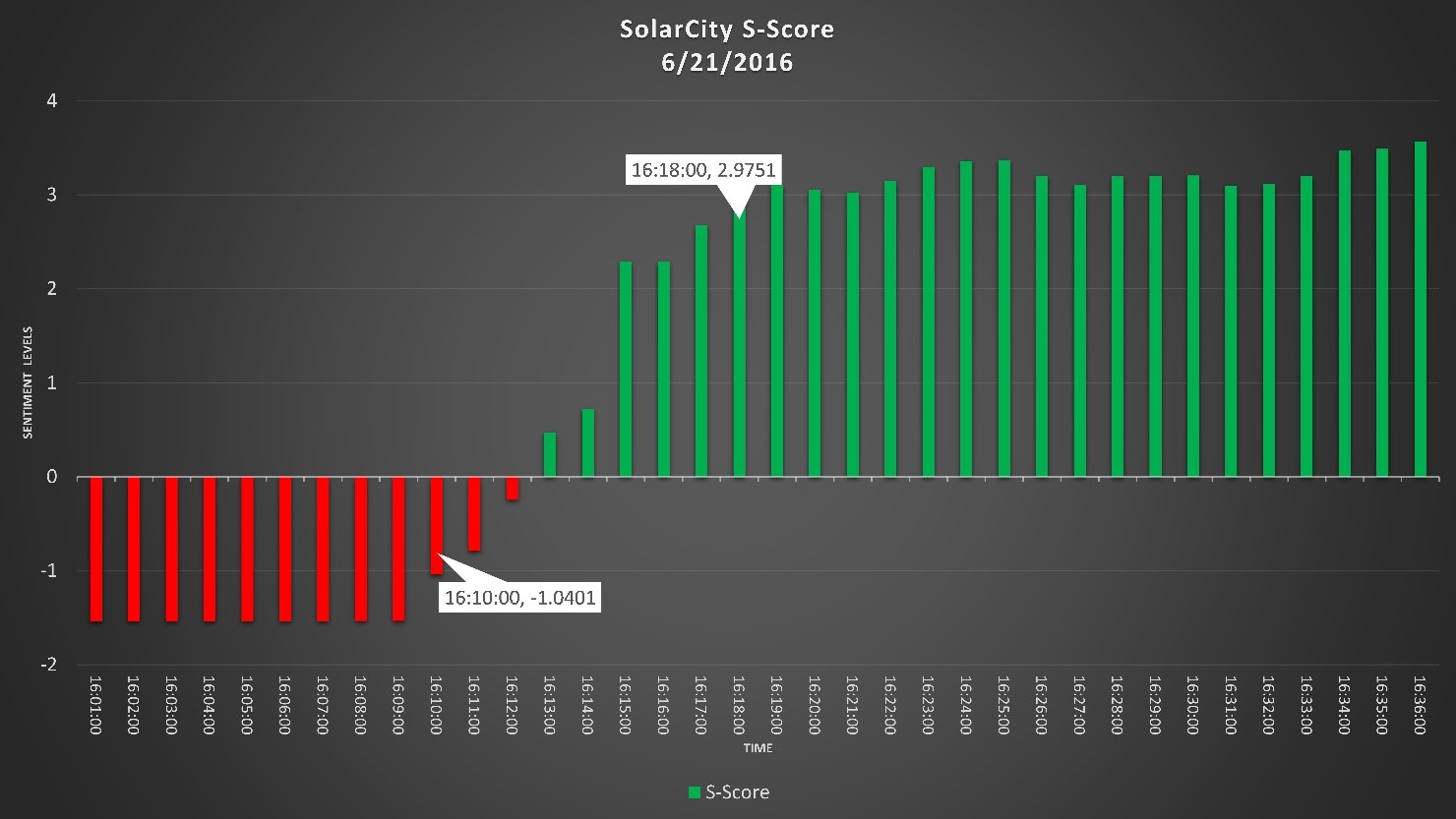

Tesla Motors lit up Twitter, yesterday, when CEO, Elon Musk came out and said their cars can float on water. Tuesday June 21, the electric car manufacturer took everyone by surprise when they announced their decision to buy the solar panel company SolarCity (SCTY) minutes after the markets closed. The first news article to mention this came out at 4:18 PM CDT. Twitter had already gotten wind of this development 8 minutes prior with a tweet from the account “TopstepTrader”.

![]()

The tweet from “TopstepTrader” was deemed to be credible by Social Market Analytics’ sophisticated algorithm, which separates signal from noise to create actionable intelligence. The sentiment started to move in a positive direction the very next minute. By 16:12 CDT, SMA’s subscribers received ‘S-DeltaTM’ alerts on SCTY. The PredictiveSignalTM from SMA became positive at 16:13 CDT and at 16:18, when the first news article came out, the sentiment had already reached an extremely positive level, with Tweet volume soaring high; as was the stock price. Traders who incorporated social media sentiment from SMA into their trading models were ahead of the curve, making profits as the rest of the market was just learning of the news.

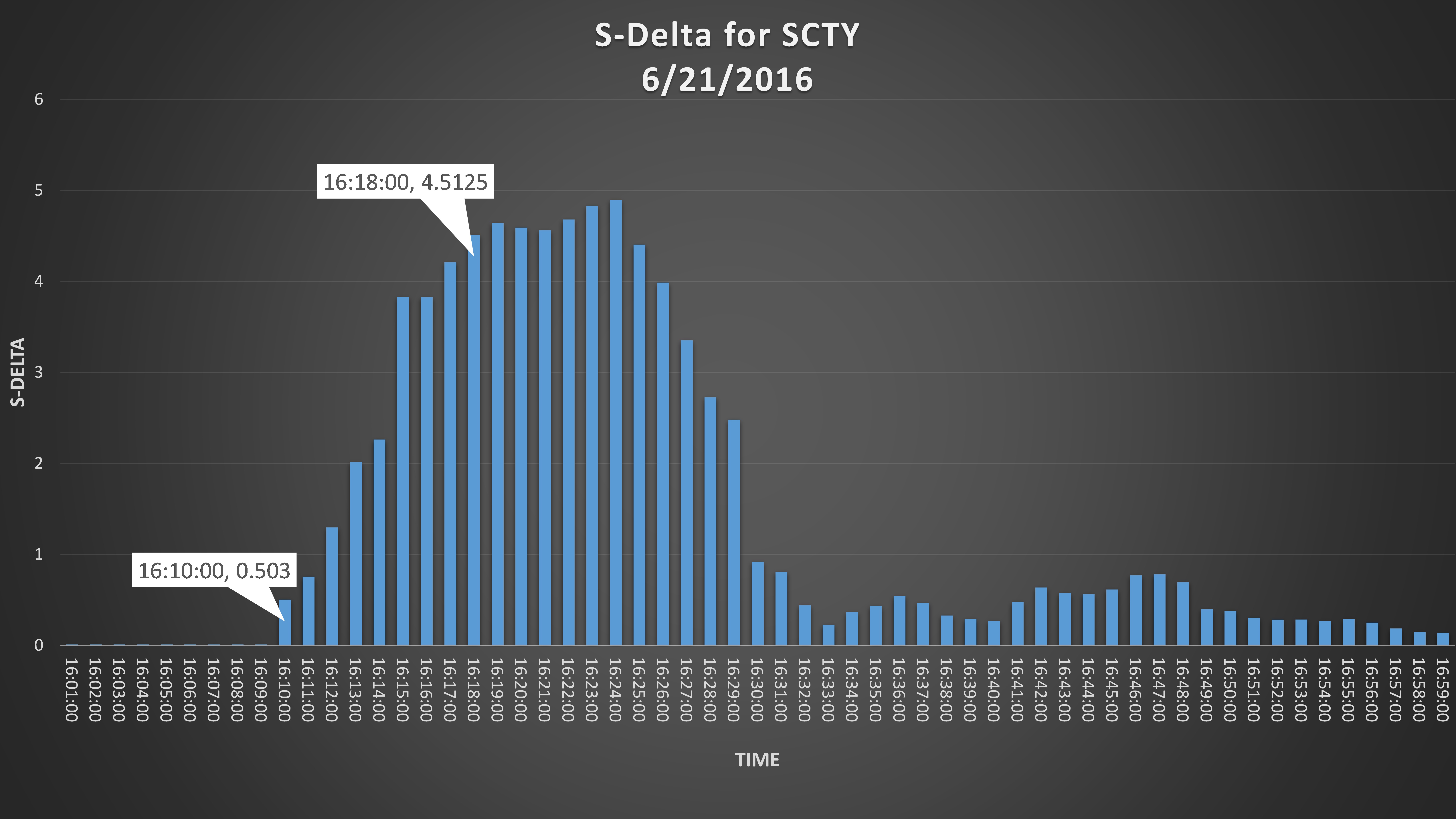

The S-Delta metric also flagged this move. The below chart illustrates the delta values for SCTY. Delta represents the change in S-Score over a 15 minute lookback. Delta values of 2 or higher are huge outliers. An SMA alarm based on Delta or S-Score would have provided an alert to this breaking news.

To find out how you can use SMA S-Factors in your investment process contact us at Info@SocialMarketAnalytics.com

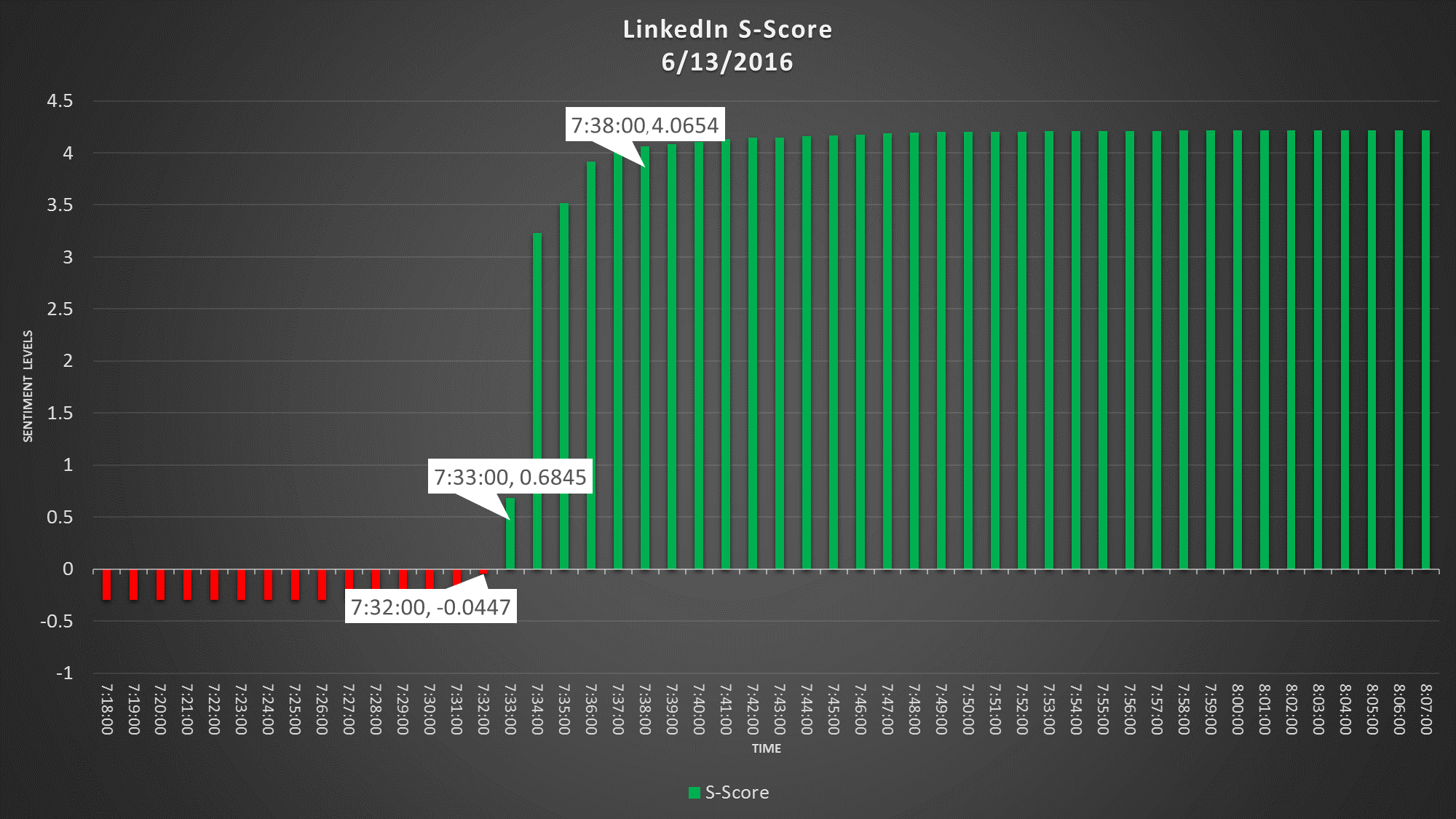

As is the case with most corporate events now, MSFT buying LNKD broke on Twitter first. The very first mention of this is any news article was at 7:38 AM (CDT) but Social Market Analytics (SMA) detected this 7 minutes ahead at 7:31. SMA’s patented algorithm digests, filters and evaluates Tweets in real time. The filtering process, a proprietary Tweet account filtering technology built by SMA, separates signal from noise by continuously scanning for accounts that are deemed credible to be included in the calculation process. The tweets from spam accounts are filtered right away.

The following are the 5 tweets that SMA received from these credible accounts in a matter of 13 seconds. All of them pointing towards the same positive news.

The 7:32 AM sentiment, as a result, had already started moving positive. By the next minute, at 7:33 AM the sentiment was already positive and soaring up. By the time other news sources caught up to this news, at 7:38 AM, the sentiment was already very positive. The S-DeltaTM alerts which measures the 15 minute changes in the sentiment had started firing up at 7:33 AM as people took notice of this and the Tweet volume kept soaring.

Contact SMA for more information about using Twitter based metrics in your investment process: info@SocialMarketAnalytics.com

Signals derived from Twitter data have typically been viewed as shorter term signals. There are a number of reasons for this. One reason is the lack of out of sample data to back test trading systems on. At SMA we now have nearly four and a half years of sentiment metrics to use in the creation of longer term signals. Long-Term is a subjective term when discussing holding periods. For our purposes we will be looking at trading signals that generate an average holding period of one month to three months.

At SMA we do not believe that one metric provides the full tone and context of a Twitter conversation. That is why we publish a family of metrics call S-Factors that provide a richer view of the conversation than what is available with a single metric.

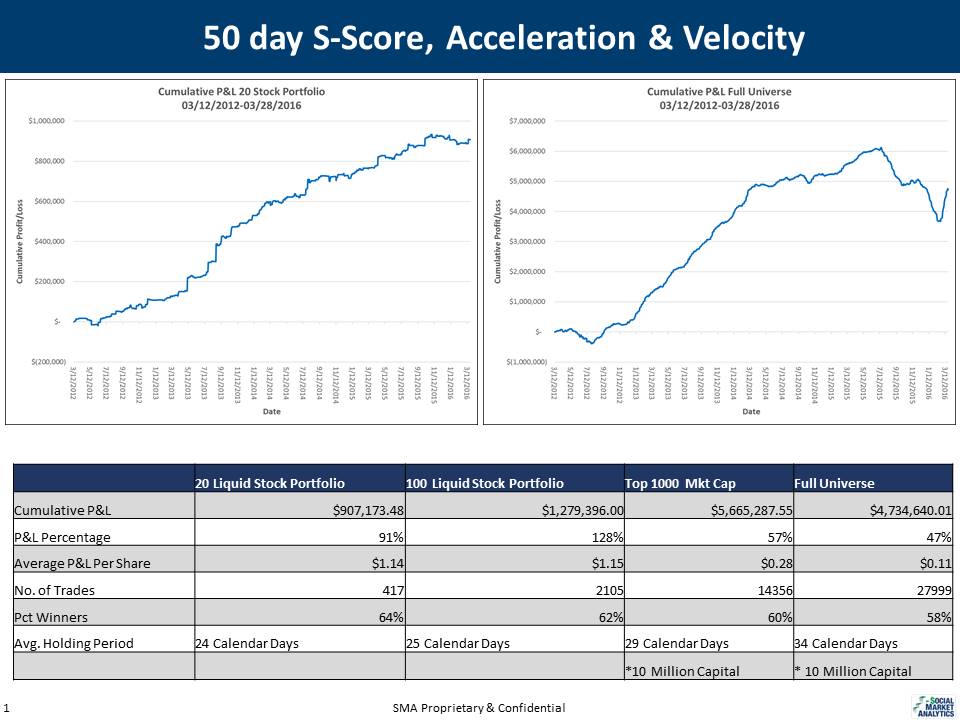

With history we have been able to look at longer term metrics and changes in security prices over longer periods. We looked at large rapid negative changes in sentiment and determined that these sentiment movements are overreactions and lead to buying opportunities. We introduce two new metrics: Velocity and Acceleration. The universes for these back test range from 20 large Twitter followed liquid stocks to the entire equity universe. As you can see below these strategies identify solid buying opportunities and generate healthy average profit per share. Please contact SMA to learn more about using sentiment to generate longer holding period trading signals with sentiment data.

Below are equity curves and trading statistics net of commissions with various universes. Overall you generate much fewer trades and hold them for longer periods of time. The 50-day S-Score chart uses the SMA S-Score, Velocity and Acceleration Metrics. You see that the holding periods are much longer than signals typically generated by social media. The columns represent different universe sizes.

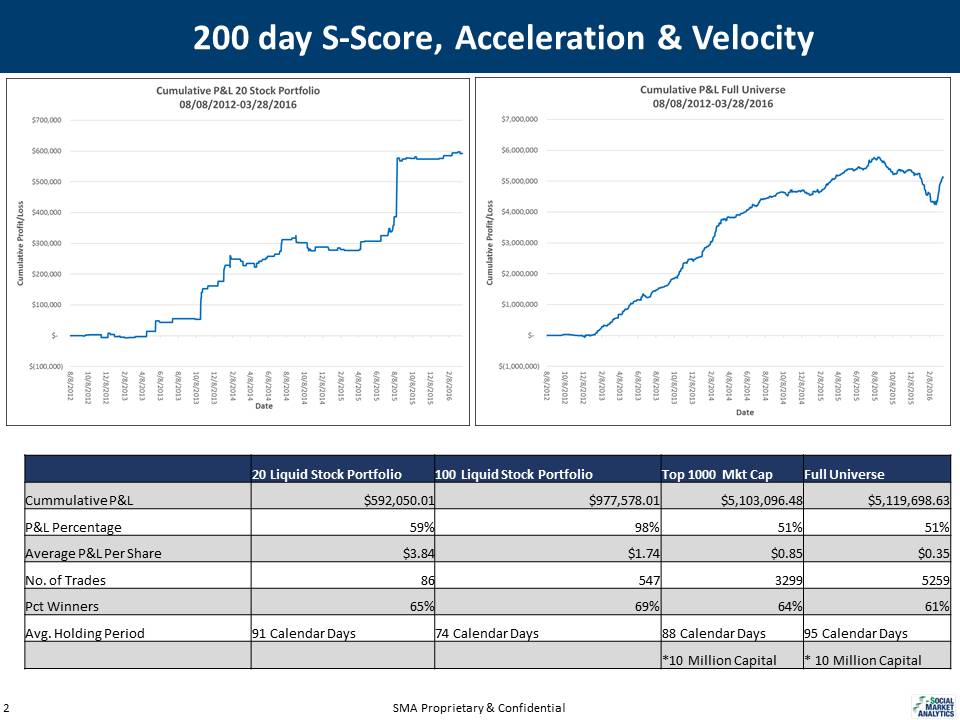

200 Day S-Scores returns are below. Again, please contact SMA for more detailed information.

To learn more please contact us at: ContactUs@SocialMarketAnalytics.com

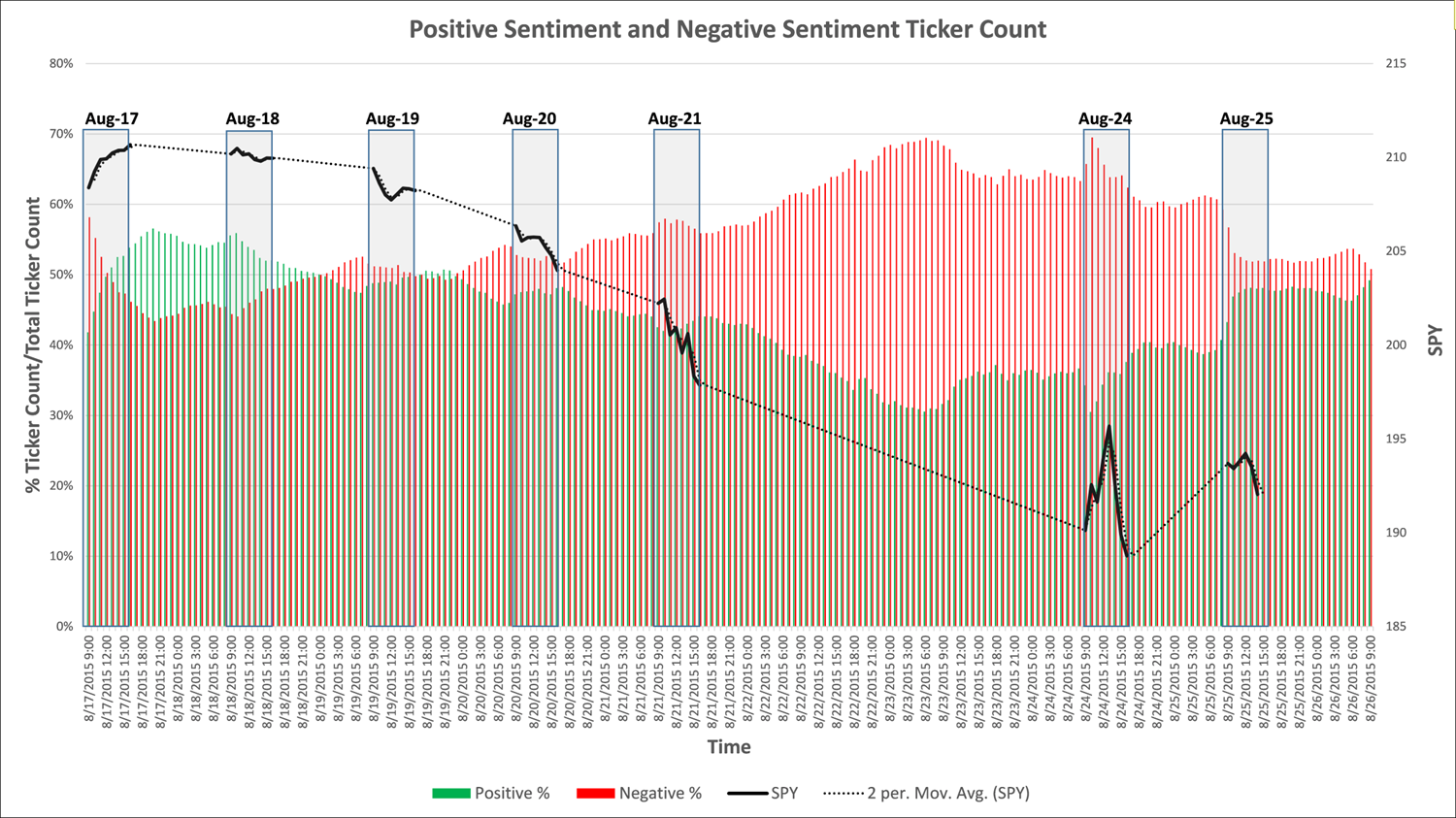

The chart below looks at the percentage of positive Tweets versus the percentage of negative Tweets over the last couple of weeks. There are usually significantly more positive than negative Tweets so the fact that the negative percentage was so high is valuable data in itself. As you can see the percentage of negative Tweets increased prior to days with significant market downtrends.

The black lines on the chart represent market activity. The red and green bars represent negative and positive Tweet percentages. Sentiment is captured by Social Market Analytics 24×7; you can see the growth in negative sentiment prior to the Monday (8/24 draw down). On 8/24 the market started strong and fell significantly at session end.

The universe of Tweets is so large that when you aggregate it you get a terrific view of what people believe is going to happen. This data is only available from Social Market Analytics. Please contact us for more information on our market leading data sets or visit our Research Page.

Thanks,

Joe

Every quarter we review performance returns and statistical ratios for our family of S-Factors. S-Score is a normalized representation of sentiment over a pre-defined look back period and is a key metric. Below are some charts that look at the full history and YTD performance of our data across the entire universe.

Anyone can pick specific securities and instances where sentiment leads price movement; it’s a lot harder to consistently predict movements over the entire universe over a long period of time. We pride ourselves on statistical consistency of our data over what is now 3.5 years of history. We are the only company to track and publish these metrics, providing the most transparency.

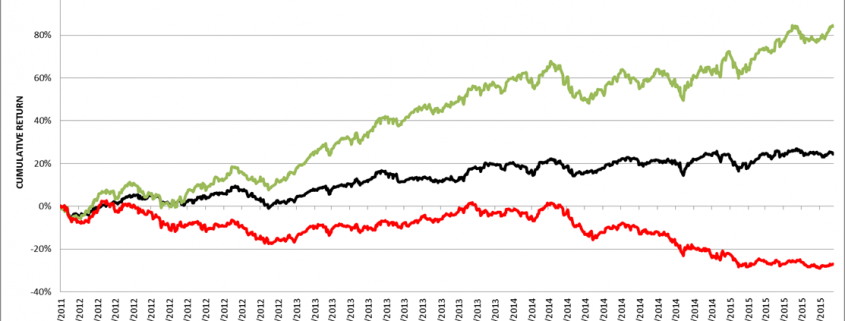

We view S-Score >2 and S-Score <-2 as statistically significant. An S-score of 2 means the current conversation on social media is more positive than 97 percent of prior conversations as filtered by our proprietary metrics. When this happens the security moves higher with statistically significant consistency. The green line below represents the full history cumulative open to close return chart of stocks with a high S-Score (S-Score >2) prior to market open. The Red line represents the full history cumulative open to close return of stocks with an extreme negative S-Score (S-Score <-2) prior to market open. The black line represents the open to close return of stocks in the SP500. The Sharpe and Sortino ratios for the green line (Pre-Open S-Score >2) are 1.37 and 2.23 respectively. Sharpe and Sortino ratios for the red line (Pre-Open S-Score <-2) are -.54 and -.86. Benchmark SP500 Sharpe = .69 and Sortino = 1.08.

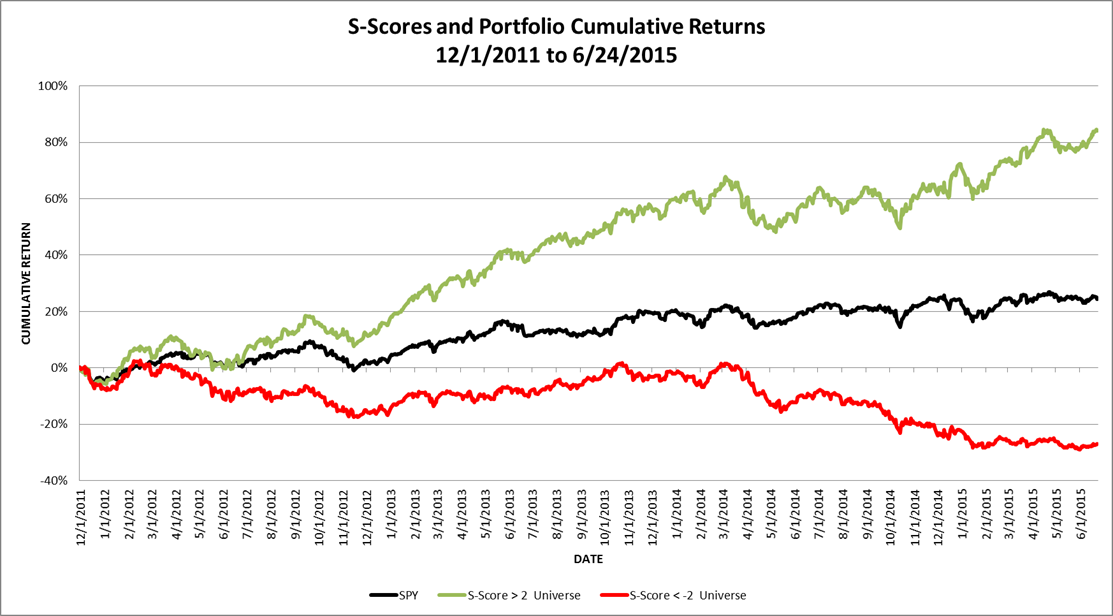

Below is the exact same chart for YTD 2015. Sharpe and Sortino ratios show the benefit of our evolving filtering and scoring criteria.

Price and Tweet volume filters are commonly added when filtering stocks for sentiment. Tweet volume represents indicative Tweet volume, once all Tweets are filtered indicative volume typically represents only 10% of the total volume of Tweets. The below chart is the same return chart represented above with the added filter of Price day close price >5 and indicative Tweet volume > 5. As you can see the Sharpe and Sortino ratios increase dramatically by adding simple filters.

Social media analytics is a learning process. Our filtering and cleansing algorithms are continuously evolving. We maintain our history as it was at each time and we keep dictionaries and accounts as a time series.

We have many more statistics employing other S-Factors and filtering criteria; please contact us for a more detailed briefing on SMA data and products.

Thanks,

Joe

SMA is an analytics company with unique IP for filtering and quantification of social media. SMA to date has been primarily focused on the capital markets given our extensive knowledge of this industry. On deck for us is the natural expansion of our capabilities to a “Topic Model” format. Right now, we use our proprietary technology to filter and quantify the conversations around stocks, commodities and foreign exchange. But the world cares about much more and we can help.

Early on we recognized the trans-formative value of Twitter as the next frontier for breaking and disseminating news. Its high noise to signal ratio represented an opportunity for us to apply our knowledge to generate value. We founded SMA in early 2012 to help people in the capital markets make sense of Twitter without having to weed through individual tweets. We could see the explosive growth trajectory of tweets – now at 750 million a day – and realized it would soon become impossible to use traditional tools to really understand the market pulse around these social conversations. We learned to convert the Twitter fire hose into real-time streams of high signal predictive data. We also learned that the methodology used to generate these data streams let us filter the fire hose for specific conversations in very valuable ways.

First, we filter accounts for quality based on programmatic algorithms. We started this process to eliminate the spammers, scammers and pump-and-dump schemers. It’s a critical step in finding the quality information. Even with this filtering, we current certify 65,000+ Twitter accounts for capital markets conversations alone, more than one person could reasonably manage to follow. Each approved account is then rated and weighted, again diagrammatically. This step is interesting for a Topic Model format in that you can certify accounts for different topics to create an expert stream of signals on any topic.

Next, we generate our S-Factor metrics. SMA Dashboard Clients are familiar with our S-Factor Alerts. Let’s talk about what these can really do. Let’s say you’d like to track conversations on new products, but you really only need to know when the excitement is extremely high/low, rapidly turning negative, very volatile or going viral. By building a list of custom alerts on your specified Topics, you get only what you want, when you want it. If you want to know of the slightest hint of trouble, you can specify tight thresholds. Or you can set your threshold levels much higher and only get notified of extremely unusual conversation trends. You can then drill down to the individual tweet level to get more granular level content. You can also search on individual tweet scores and view just those tweets with high/low scores.

SMA will send you an e-mail or text alert when your specified alert limits are hit. You can also track all changes in real-time on the Dashboard. Of course, we still have our high-powered API and all of this capability can be directly integrated into any client system. From the start, we designed our technology to be source and search agnostic and given client demand, we’ve added additional data sources. As we start tackling the conversations outside of finance, we welcome your interest in new Topics.

By Kim Gits, CFO

By Kim Gits, CFO of Social Market Analytics

Are you prepared for the shift in attitudes and expectations of the next generation of investors? What is the next step for social media use in the capital markets? How far will you go in implementing a social strategy to retain/attract investors? Once in house, how will you communicate with them?

Much has been said about this new generation of investors – the Millennials. Their generation is larger than even the Boomer generation. They will be recipients of the largest wealth transfer in history. They grew up with cellphones and instant access to information via the internet. They are social and mobile.

But what does this mean to firms who wish to court this generation of investors?

In the last few years, we have seen Twitter and other social media sites like StockTwits and Seeking Alpha come of age as reliable data sources. At Social Market Analytics, we are incredibly excited about these questions and the changes in investing that are on the horizon.

I’d break down the market response to this paradigm shift in waves. The first wave many years ago was to develop a consistent firm-wide policy for employee use of social media. Much legal angst went into creating these edicts. Many of the Boomer and even GenX population saw it as a fad that would pass and certainly never saw themselves as Twitter users (Deja-vu for me when thinking about the adoption of the internet in the late 80s). This first wave marked the beginning of a new means of communication. For us at SMA it represented a new source of data as “smart money” finally had the clearance to Tweet their thoughts.

I’d describe the second wave as the re-posting of individual Tweets – something we began seeing as early as 2012. A few firms began streaming Twitter posts as they related to stocks and the markets. But let me ask you – with over 500,000 tweets, about stocks, a day (and growing) is it really possible to read all of those Tweets and still get any work done? Do you really care that your brother-in-law’s third cousin thinks Apple is going up (unless of course he’s Warren Buffet)?

The third wave was adoption of social media data by hedge funds and quant traders. Always on the lookout for new ways to generate alpha, this group has been adding various forms of social media data to their trading strategies. SMA and its partners have been at the forefront of research in alpha generation strategies using S-FactorsTM, our social media metrics. Growth at this level continues with more advanced strategies using multiple asset classes.

The final wave as I see it is the native integration of social media and its rich knowledge sharing capabilities into the investing platform. Not only will investors be alerted to what they want to know in real-time, they will also have the ability to communicate socially with their brokers and execute transactions on a mobile platform based on either alerts or social communications from their broker.

As you address these coming changes, we are prepared to help. SMA finds the real-time “smart-money” conversations in social media. Knowledge sharing is known to be important to this new generation of investors. SMA’s differentiation is that our proprietary filtering eliminates the spammers, scammers and naïve-user conversations. Our metrics are based on the social media posts of “smart-money”. Also, SMA’s unique normalization process helps users find hidden stock conversations that might otherwise be overwhelmed by the likes of Apple, Google and Facebook. Our data and metrics are engineered to perform at the highest levels and we offer fine-grained customization to meet the needs of your specific customer base. User-defined thresholds of our metrics let investors listen to only the conversations that are meaningful to them. To learn more, please contact us at info@socialmarketanalytics.com

Thanks,

Kim

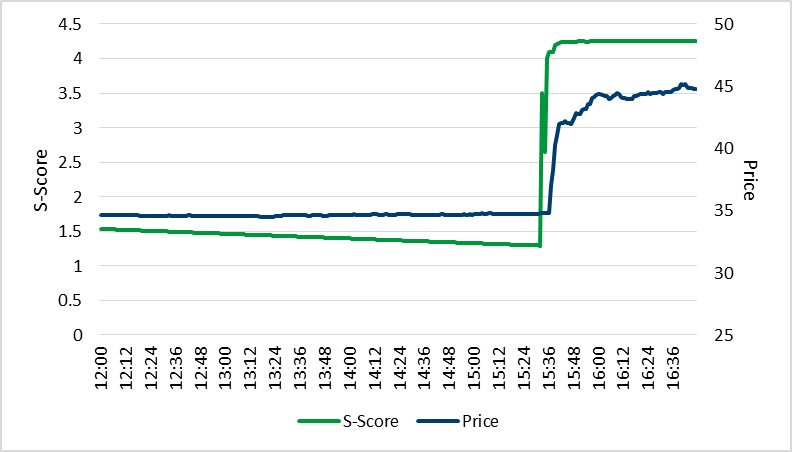

There is a rapidly growing consensus in capital markets that rigorously analyzed information derived originally from social media can be a very valuable input in identifying trading opportunities. Nowhere was this more evident than in what happened to Altera shares on Friday, March 27th. Once news broke at 3:32 PM EDT in a Tweet by a respected Wall Street Journal reporter that Intel was in talks to buy Altera, share prices began to skyrocket…so much so that trading in Altera was halted after only three minutes at 3:35 PM. The story was highlighted in a number of places including The New York Post and CNBC: http://nypost.com/2015/04/02/wall-street-trader-makes-2-4m-thanks-to-a-tweet/ http://www.cnbc.com/id/102545580 But within that very short window a savvy options trader was able to put in a bid for 300,000 options on Altera at $36 per share. At the closing bell that Altera’s price was $44.39. The trader cleared just over $2.4 Million…not bad for an afternoon’s work. It is not clear what the exact mechanism was that enabled this trader to pull off such a spectacular trade….perhaps just great timing, perhaps using some sort of sophisticated model that incorporates input derived from conventional news sources and/or social media. But, what we know at Social Market Analytics (SMA) is that our analysis tracked this spectacular deal perfectly. SMA clients use our Sentiment (or S-) Factors as key inputs into the trading models they use. The graphic below illustrates what SMA analytics predicted what would happen. Tweet time is central time. Chart is based on Eastern time. Our signal reacted well before the price move.

The below chart overlays the SMA signal and price. Our SMA S-Score reacted significantly before the price changed happened. Definitely time for SMA customers to act!

This functionality is only available through SMA – Contact us for more details. Thanks, Joe